Although US President Donald Trump did not label China a “currency manipulator” on his first day in office as he said he would, a team at Deutsche Bank is not ruling out the possibility of him doing so going forward.

“Some time in the next couple of weeks, we think it is likely that President Trump will declare China a currency manipulator and propose penalties if it does not enter into negotiations to lower its trade surplus with the US,” the team led by Michael Spencer, chief economist at Deutsche Bank, wrote in a note to clients last week.

“This has been a consistent campaign promise and he has demonstrated since taking office his determination to deliver on his promises, however controversial,” they continued. “Existing US law and its application by the Treasury in recent years are unlikely to satisfy the President’s desire for strong penalties for unfair trade, so we anticipate that the proposed measures could go far beyond what has thought possible even a few weeks ago.”

China has been trying to control the rate of its currency’s depreciation since 2014, and it has had a harder time keeping it stable in trade-weighted terms since mid-2016.

Policymakers have reversed previous trends of capital account openness and currency internationalization in an attempt to slow the pace of the yuan’s depreciation. Additionally, foreign exchange reserves have depreciated as they attempt to support the currency.

As the Deutsche Bank team noted regarding this: "While this intervention policy can indeed be described as 'one sided' as proscribed by US law, it is intervention in the direction that would normally be viewed as in the US' interest - to prevent even faster depreciation of the Chinese currency."

Notably, there are three criteria that must be met for a country to be labeled a currency manipulator by the Treasury Department:

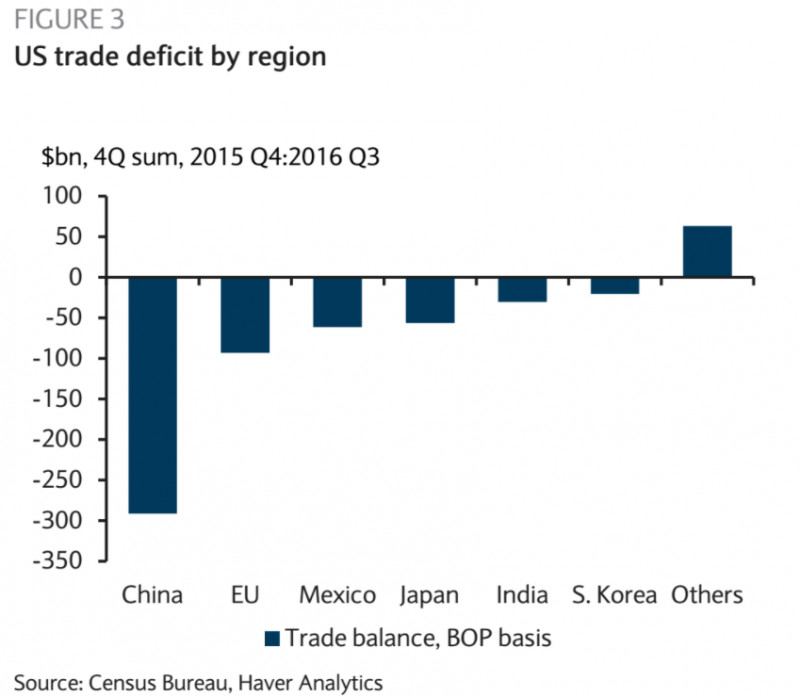

The country must have a significant bilateral trade surplus with the US. The country has a "material" currency account surplus. The country is engaged in persistent one-sided intervention in the foreign exchange market.

In their semi-annual April report, the Treasury created a "Monitoring List" of major trading partners that "merit attention based on an analysis of the three criteria." Once a country is added to the list, it is kept on there for at least two consecutive reports.

China was among those added to the list. However, the Treasury noted that while it met two out of the three criteria in the April report (a large bilateral trade surplus and a current account surplus above 3%), it met only one of the three criteria in the October report (the large bilateral trade surplus.)

As an aside, Deutsche Bank strategist Robin Winkler argued that, actually, the country that is the closest to meeting the Treasury Department's three criteria is Switzerland.

In any case, going forward, if Trump does label China a "currency manipulator," the follow-up question becomes: how will China respond? Again, here is what the Deutsche Bank team thinks (emphasis added):

"In the trade policy realm, the authorities have signaled that they'll respond with tariffs in proportion to the US move. So a sector-by-sector application of anti-dumping tariffs, for example, will likely be met by a similar response from China. An across-the-board tariff on all imports from China would likely be met by a similar response on the Chinese side.

But we think China's currency policy is unlikely to change materially in the event it is labeled a currency manipulator. We do not expect them to refrain from intervening and move to free float - which would likely lead to a large depreciation - nor would we expect a one-off devaluation. The authorities have had three years to allow a large sudden depreciation and even the modest 3% devaluation in August 2015 seems to have been too much volatility for them. At most, a controlled depreciation such as we observed in the first half of 2016 would be possible, in our view."

For what it's worth, the last time the US designated China a currency manipulator was from 1992 to 1994.